Everything you need to know about the new Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS)

This year over 50,000 businesses across the European Union will be affected by the new Corporate Sustainability Reporting Directive (CSRD).

But what exactly is it and how will your business be affected if you trade in Europe?

CSRD explained

CSRD, is a new directive outlining how organisations must report on their environmental, social, and governance performance.

It replaces its predecessor, the Non-Financial Reporting Directive (NFRD) and aligns with the Net Zero goals set by the European Green Deal. CSRD will also provide transparency to investors and other stakeholders on the sustainability risks they have a right to know about.

What is ESRS?

CSRD is based on the European Sustainability Reporting Standards (ESRS for short and not only is it a mouthful, it’s over 250 pages long). Similar to financial reporting, these standards offer a uniform approach for all companies to comply with the new reporting.

They are comprehensive and rigorous, covering everything from general requirements to human rights, ethics, climate change and sector-specific topics related to biodiversity, supply chain management and circularity.

These standards will ensure consistent reporting and the ability to compare ESG progress across multiple industry sectors.

Double Materiality

The first crucial step of the CSRD reporting process is to conduct a double materiality analysis on the business. This analysis is essential for assessing how sustainability issues affect both the company's bottom line and its broader impact on people and the planet.

These two impact perspectives are categorised as:

Outward Impact: A company's actions on both people and the planet over the short, medium, and long term, not only within your operations but also throughout your entire value chain.

Inward Impact: How sustainability issues impact your business financially, looking at factors such as growth, performance, and cost of capital across the short, medium, and long term.

In essence, a double materiality analysis helps identify and prioritize the issues that are most relevant to the business and its stakeholders. In turn, it will enable businesses to determine what should be included in their CSRD report, aligning with both the general requirements and specific disclosures needed.

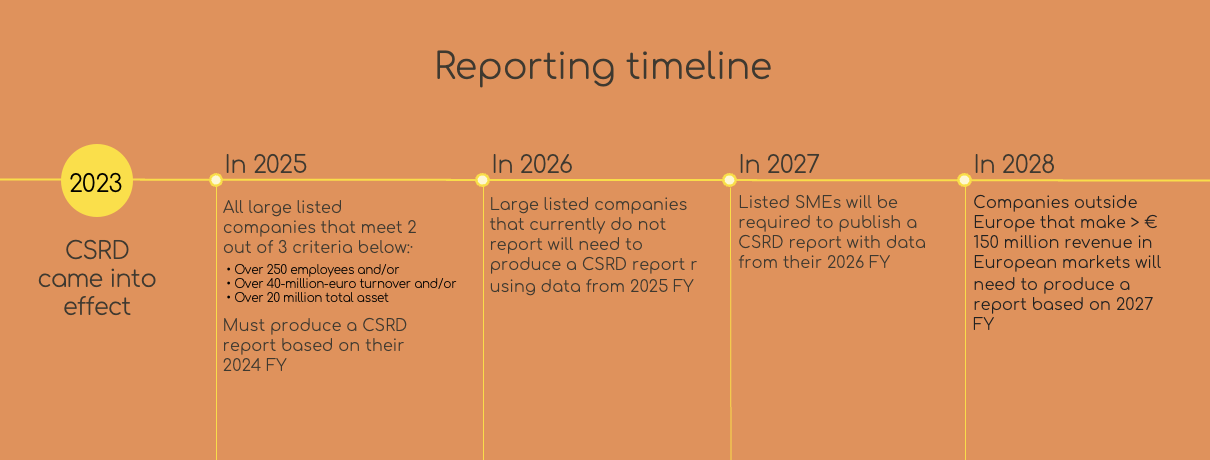

When do you need to start reporting?

We will start to see the first official CSRD reports in 2025, as all large listed companies that meet 2 out of 3 criteria below must produce a report based on their 2024 financial year.

· Over 250 employees and/or

· Over 40-million-euro turnover and/or

· Over 20 million total assets

In 2026, large listed companies that are currently not required to report on non-financial data will need to start publishing their first CSRD report with data from their 2025 financial year.

In 2027, listed SMEs will be required to publish their first CSRD report with data from their 2026 financial year.

Who needs to be involved?

Stakeholder engagement lies at the core of CSRD and demands collaboration across all organisational levels. From the C-suite to operations, from HR to procurement, active participation throughout the organisation is vital because data collection, monitoring and reporting spans across all departments.

Your 6 CSRD need to knows:

1. Annual Reporting: Companies must produce a report each year following ESRS guidelines.

2. Phased Rollout: The directive will be introduced gradually over the next few years, starting with larger companies.

3. Double Materiality Assessment: This first crucial step is required as part of the process.

3. Third-Party Audit: Companies need a credible third party to verify their sustainability data.

5. Full Reporting: CSRD requires reporting on the entire value chain, not just a company's own operations.

6. Due Diligence Disclosure: Companies must share details of their due diligence processes and findings.

CSRD is a tool for a fairer, equitable, sustainable future

In essence, the CSRD isn't just extra paperwork; it's a game-changer for Europe's sustainability. By promoting transparency and action, it's not about checking boxes; it's about making a real difference.

Let's see it as our tool to drive change, paving the way for a better, equitable, sustainable future for everyone.

We are accredited to implement CSRD

We are accredited in CSRD implementation and specialise in supporting businesses through the entire CSRD process from start to finish. From conducting the crucial double materiality analysis to ensuring all the required disclosures from the European Sustainability Reporting Standards (ESRS) are included in your final CSRD report.

If you're interested in delving deeper into CSRD or require assistance with your report, why not schedule a complimentary 30-minute consultation through our Calendly?

Alternatively, feel free to reach out to our CSRD expert, Jenn, at jenn@cydconnects.com with any inquiries.